The buzz picked up over the summer around how dealflow is improving; even predictions for record totals in the year ahead. But like footprints in wet cement, the numbers don’t lie, and middle market dealmaking in August is showing no signs of moving forward yet. Nonetheless (and yes, you’ve read it here before), dealmakers insist that momentum is building up for what should be a busy fourth quarter. Here’s our monthly deal analysis.

“We see momentum building toward Q4,” says Jeff Buettner, a managing director at ButcherJoseph & Co. “With 2025 winding down, buyers, private equity and strategics alike, will be increasingly motivated to wrap deals before year-end closing deadlines. Expect continuation of creative structuring: earnouts, seller notes, minority recaps, or even ESOP or deferred liquidity models, as buyers and sellers work to reconcile price and value. Businesses that can clearly demonstrate resilience through inflation, labor pressures, and capital discipline will stand out and attract premium valuation multiples.”

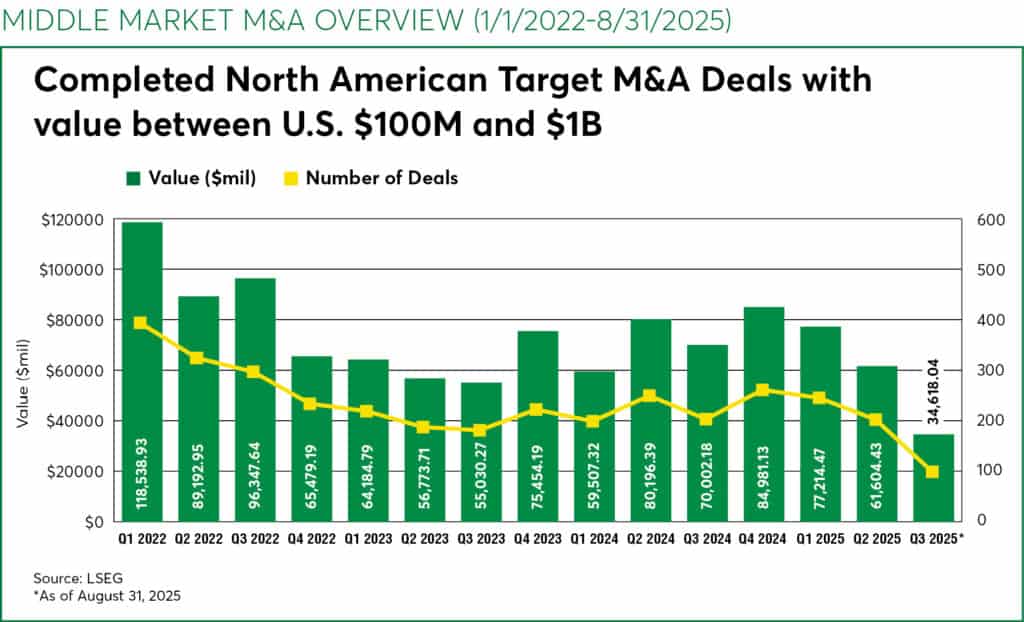

The August numbers are not pretty at all. According to data provided by LSEG, August saw just 35 mid-market deals valued at around $10.15 billion. That is about half of the 69 deals closed, worth around $24.2 billion in August 2024. The data is based on North American completed deals worth between $100 billion and $1 billion. It’s by far the lowest monthly total recorded post-Covid.

Year to date, as of Aug. 31, there were 576 deals worth around $173 billion compared to 620 deals worth around $190.1 billion through the same time period last year.

Looking at specific sectors, real estate is the most active thanks to demand for data centers. The real estate sector saw 83 deals closed through August 31, valued at around $20.4 billion, compared to 37 deals worth about $9.7 billion through the same time period one year ago.

Technology is the other sector showing positive momentum, driven by AI, with 149 deals announced so far this year worth $38.2 billion compared to 138 deals valued at around $37.7 billion through the same time period last year.

Healthcare continues to lag mightily seeing only 74 deals valued at about $20.2 billion so far this year compared to 116 deals valued at around $29.5 billion from the same time frame last year.

Energy, consumer staples and retail are also down significantly this year with 53, 9 and 6 deals, respectively, compared to 73, 19 and 15 deals from last year.

Notable deals that closed in July include Elf Beauty’s (NYSE: ELF) purchase of HRBeauty and Granite’s (NYSE: GVA) acquisition of Warren Paving.

In the league tables, Goldman Sachs (NYSE: GS), JP Morgan (NYSE: JPM) and Evercore (NYSE: EVR) hold the top three spots by advising on the most deals so far this year (36, 29 and 22, respectively.)

Despite the ugly numbers, dealmakers insist deal activity will pick up this year. “We remain cautiously optimistic that the momentum built in Q3 will extend into Q4 and early next year,” says Wiggin and Dana Partner Andrew Ritter. “While some headwinds, particularly geopolitical uncertainty, may temper the pace of activity, the market has shown encouraging signs of resilience.”

See the full list of August’s biggest mid-market deals here.