Data centers are emerging as the newest anchor for secondaries growth and GP-led investors are increasing their underwriting before buying.

AI’s Secondaries Moment

The private equity industry’s next major continuation vehicle boom may not come from consumer brands, healthcare roll-ups or software platforms. Instead, it will stem from the physical infrastructure that underpins artificial intelligence.

As sponsors race to build exposure to data centers, fiber networks, power assets and cooling infrastructure tied to the AI buildout, a growing number of firms are confronting the same problem plaguing PE: they do not want to sell their best-performing assets into a market they believe could still reprice materially upward. Yet, they still need to generate liquidity for LPs after years of muted distributions.

The result is creating fertile conditions for a new wave of AI-linked GP-led secondaries transactions.

PJT Partners predicts the market will nearly double to $45 billion in 2030 compared to the $25 billion transacted last year.

Advisers, sponsors and secondaries buyers alike are preparing for what many expect will be a significant increase in AI-related GP-led deal activity. Evercore, the undisputed leader in CV advisory, recently announced it had poached Campbell Luytens infra secondaries head Clay McCoy to beef up its own unit dedicated to the asset class.

Real-world transactions are already emerging. Last year, GI Partners moved data-center operator Flexential into a $1 billion CV, anchored by Hamilton Lane (NYSE: HLNE).

Meanwhile, Blackstone (NYSE: BX) has become one of the most aggressive investors globally in AI infrastructure. The $1.3 trillion titan recently announced a $5 billion joint venture with Google focused on TPU cloud infrastructure.

Blackstone also closed the largest fund dedicated to the asset class at $5.5 billion in September. Ardian is closing in on a similar amount for its infra secondaries fund, while Ares (NYSE: ARES) closed its $3.3 billion Secondaries Infrastructure Solutions Fund III in October.

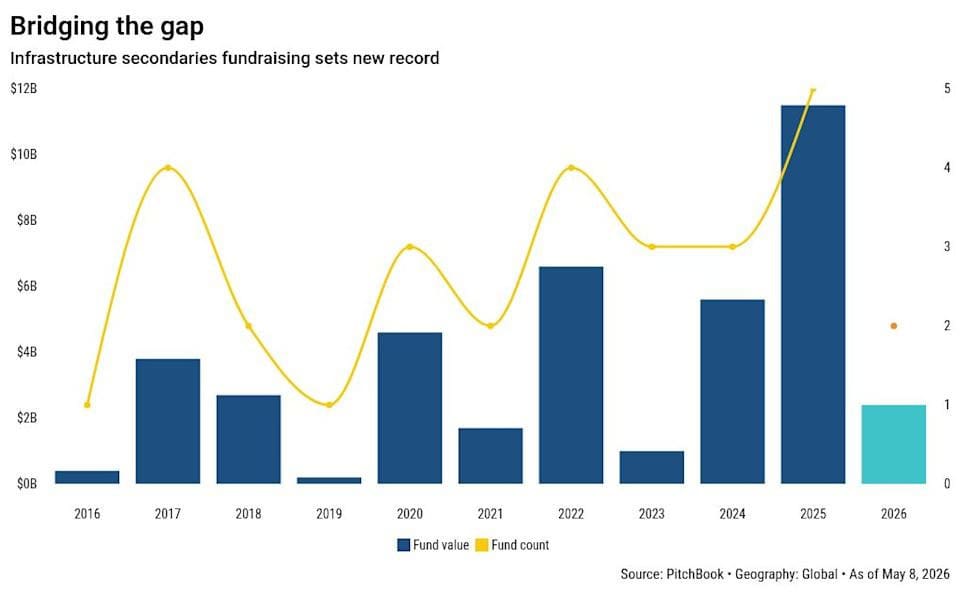

Fundraising for the asset class reached a record $11.5 billion last year, more than doubling the $5.6 billion raised in 2024, according to Pitchbook.

Takeaway: Infrastructure has emerged as one of the fastest-growing categories, representing nearly 15 percent of total secondaries deal flow, as investors gravitate toward established, cash-generating assets in a higher-rate environment. And in the AI era, continuation vehicles may emerge as one of private equity’s preferred ways to hold onto the assets it least wants to sell.

Big Data

Infrastructure secondaries fundraising is rapidly emerging as one of the hottest corners of the broader private-markets liquidity boom, driven by a fundamental mismatch between the lifespan of infrastructure assets and the traditional 10-year structure of private funds. Fundraising for dedicated infrastructure secondaries strategies reached a record $11.5 billion globally last year, more than doubling from $5.6 billion in 2024, according to PitchBook data

The market’s growth is being fueled by both structural and cyclical forces. Infrastructure assets such as data centers, fiber networks, renewable energy platforms and transmission systems often require decades — not years — to fully realize their value creation potential. At the same time, many infrastructure funds raised during the post-2017 fundraising boom are now approaching maturity, creating pressure on sponsors to generate liquidity while still retaining exposure to long-duration assets.

Beyond the Bid

The secondaries industry has spent three decades telling investors it is a financial market, not an operating one. That pitch is quietly changing.

As single-asset continuation vehicles become the dominant growth engine of the secondaries market, the largest buyers are building internal capabilities that look less like a fund administration function and more like a traditional buyout firm’s portfolio operations team. Operating partners, sector specialists and value creation executives are increasingly appearing on secondaries firm org charts, hired to do something secondaries investors have historically left entirely to the GP: help the underlying company actually get better.

Single-asset continuation vehicles accounted for 89 percent of GP-led volume and 43 percent of total secondary market volume in 2025. Most of those transactions involve mature businesses with long runways for operational improvement rather than near-term exit readiness. As a result, secondaries firms are increasingly underwriting the same operational questions that traditional buyout sponsors face.

Firms that once focused primarily on portfolio analytics and liquidity underwriting are increasingly adding operating executives, sector specialists and value-creation professionals more commonly associated with mainstream buyout shops.

Ardian, for instance, has built a dedicated operations unit it calls the Value Enhancement Team within its secondaries business. Blackstone and Lexington Partners, meanwhile, have expanded their focus on concentrated GP-led and continuation vehicle transactions that require deeper company-level operational underwriting.

The evolution reflects the growing complexity — and competitiveness — of the market. In large continuation vehicle deals, buyers are often acquiring concentrated exposure to one or a handful of companies at very large valuations. Underwriting increasingly depends on having differentiated views around revenue growth, pricing power, margin expansion and sector-specific execution.

Market participants say underwriting efforts typically still aren’t as thorough as the buyout process, but that’s changing.

Increasingly, secondaries buyers are requesting detailed operational and financial information, including customer analytics, historical financial statements, lease agreements and insurance documentation. Due diligence generally also includes management meetings, facility tours, expert network consultations and customer reference calls.

Lead CV investors are now typically building their own leveraged buyout model for the asset.

In some cases, secondaries investors are taking more active governance roles after transactions close. Continuation vehicles frequently involve extended hold periods, meaning buyers cannot rely solely on financial engineering or rapid exits to generate returns. Operational value creation increasingly sits at the center of the investment thesis.

The trend is also reshaping fundraising narratives. Large secondaries firms now present themselves less as passive liquidity providers and more as strategic long-term capital partners capable of helping portfolio companies scale through another phase of growth.

Bottom line: With hold periods averaging seven years and IRR increasingly dependent on operational execution rather than financial engineering, the pressure to look more like operators is not going away.

Transactions

- Blackstone andArdian acquired a 33-Fund LP portfolio from CPP Investments for a combined $2.9 billion in net proceeds.

- Blackstone and Halliburton invest $1 billion in Voltagrid, a data center power supplier. The transaction includes $225 million of secondary acquisitions.

- CPP Investments also offloaded $724 million in non-performing European loans to a joint venture formed by Arrow Global Group and Fortress Investment Group.

- Hunter Point Capital expands GP stakes strategy with the opening of its Hong Kong office.

- Onex reported it realized $317 million from its multi-asset CV, which includes new investors GIC, StepStone, Apollo (NYSE: APO) and Neuberger Berman.

Fundraising

- StepStone Group (Nasdaq: STEP) held its first close for its flagship secondaries fund, raising $2.2 billion. The firm also disclosed that its debut GP solutions fund has raised $200 million.

- Hamilton Lane announced it has formally launched fundraising for its first GP-led fund.

- Reality Growth launches real estate GP stakes strategy.

- Acacia Partners closed its fourth fund dedicated to CVs on $75 million.

People

- Evercore poaches Clay McCoy from Campbell Luytens to beef up infrastructure secondaries coverage.

- Andrew Olson, formerly Partner, CFO & COO at Revelation Partners, has joined Hercules Capital as CFO and head of corporate development.

- Jason Wehby, formerly CFO at HAUSER, has joined Timber Bay Partners as CFO.

- Nichole Kim, formerly Managing Director at StepStone, has joined CVC Secondary Partners as Managing Director.

- Yasuyuki Kanda, formerly Managing Director at AlpInvest Partners, has joined Campbell Lutyens as Managing Director.

- Alex Knowland, formerly Managing Director at Manulife / Comvest Credit Partners, has joined H.I.G. Capital WhiteHorse as Managing Director and Head of Specialty Finance Originations.

- Scott Lavelle, formerly Managing Director at PNC Alternative Solutions, has joined Diversified as Chief Investment Officer.

- William Boyle, formerly Managing Director at Morgan Stanley, has joined JPMorgan as Global Head of Secondary Advisory.

- Jack Porcelli, formerly Vice President at Coller Capital, has joined Fortress Investment Group as Senior Vice President.

- Mahdi Charafeddine, formerly Research Team Manager at Setter Capital, has joined NAV Capital Limited as Associate Director.

That’s the market in motion. Stay sharp and see you June 10. Until then, send tips, quips and tidbits to secondaries@themiddlemarket.