The PE Exit Bottleneck

While the M&A world of bankers, advisers and middle-market private equity firms has voiced more optimism around dealmaking, sponsors are managing their way through a backlog of companies bought during the boom years leading up to 2022.

This will be a growing problem for middle-market private equity firms at a time when businesses are no longer selling for the lofty multiples they commanded during the peak valuation years of near-zero interest rates that sparked record dealmaking volumes in 2021.

Mergers & Acquisitions looked at three key sectors that provide a cross-section of the deal economy – healthcare, tech and restaurants – and identified several noticeable trends.

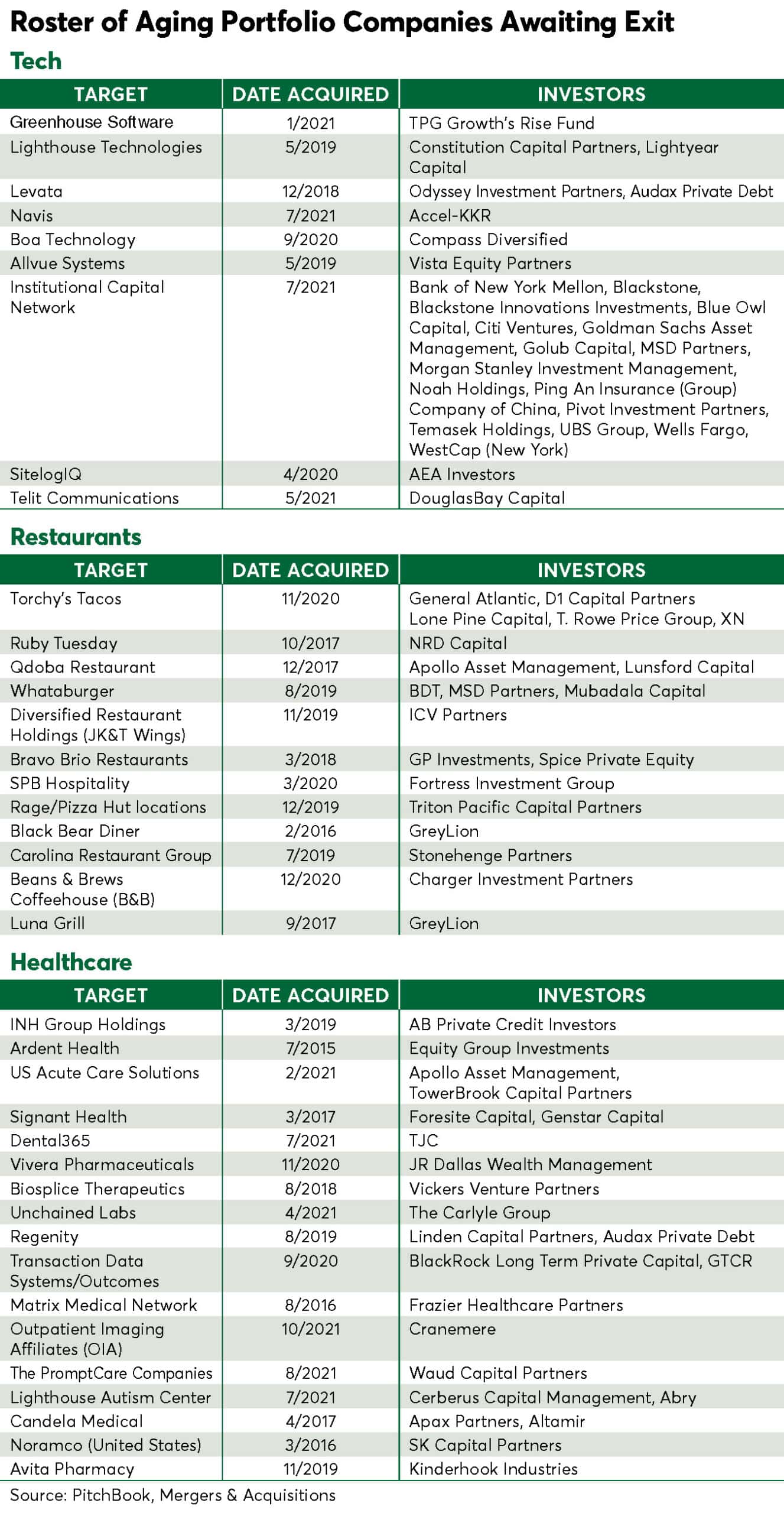

Many of the portfolio companies acquired between 2015 and 2021 were exited by 2022, but some still remain with their sponsors well past the traditional four- to six-year holding period (see charts).

Average portfolio company hold periods have increased in most sectors between 2020 and 2025. As of 2025, companies in the healthcare sector were held for an average of 6.4 years, up from 3.5 years in 2020. In business services, the average hold period in 2025 was 7.2 years, up from 6.9 years in 2020 and in energy, the average hold time in 2025 was 9.3 years, up from 5.0 in 2020 according to data compiled by Mergers & Acquisitions with assistance from Pitchbook.

The stakes are high for GPs because fund returns will sag if they sell these remaining companies at lower multiples, which in turn, could impact future fundraising efforts. The number of PE-backed companies held for five or more years without an exit is estimated at 6,000.

Companies that sold for 15x to 18x Ebitda prior to 2022 are often going for lower multiples now – sometimes 10x Ebitda or 12x Ebitda. Many portfolio companies may be overvalued if their enterprise values haven’t been adjusted to these purchase price realities.

“It’s an industry-wide problem,” said a senior managing director at a middle-market firm who has also worked as an LP, who asked to remain anonymous. “The time periods on private equity funds are ticking. LPs will want their money back, but private equity owners may be in purgatory with their portfolio company valuations.”

Each sector faces its own headwinds.

Healthcare Portcos

Healthcare portfolio companies have faced uncertainties around changing drug approval procedures and vaccine guidelines. There’s a lack of confidence in policy and regulation and this is hampering the calculation of portfolio enterprise values and growth targets.

Of the top 20 private equity deals in the sector valued up to $500 million between 2015 and 2021, just three have seen exits, according to data from Pitchbook. The 17 portfolio companies that remain under the same ownership and that have been held for more than five years include Signet Health, which was acquired for $453 million in 2017 by Foresite Capital and Genstar Capital. Others include Candela Medical, purchased for $397 million in 2017 by Apax Partners and Altimir, as well as Avita Pharmacy, bought for $290 million in 2019 by Kinderhook Industries.

Tech Portcos

In tech, AI has been disrupting services and code-writing practices.

“AI has become an unknowable force – people don’t know if they’re beneficiaries or victims,” said the PE executive. “There’s a lot of confusion around AI.”

Aging portfolio companies in the tech space include Allvue Systems, acquired by Vista Equity in 2019 for $444 million, as well as Levata, purchased in 2018 for $482 million by Odyssey Investment Partners.

Restaurant Portcos

In the restaurant space, there’s been a wave of bankruptcies in the last 12 months. The sector continues to face a loss of labor due to immigration policies and consumer affordability issues. People have even complained about $8 value meals at McDonald’s (NYSE: MCD).

Restaurants such as salad maker Sweetgreen are pivoting toward wider use of labor-saving automated systems, but these changes require capital spending commitments.

Restaurants held for several years include Black Bear Diner, which was purchased in 2016 for $77.5 million by Grey Lion.

Josh Benn, a Kroll investment banker who works on restaurant deals, told Mergers & Acquisitions recently that NPD Capital tried to sell Ruby Tuesday but was unable to do so last year. We also recently reported that AEA investors may put Jack’s Family Restaurant on the market as early as this year after a hold period of seven years.

These aren’t the only sectors where PE faces continued headwinds.

Companies in the insurance sector are facing changing patient costs due partly to lower Affordable Care Act subsidies.

Middle-market PE firms have also invested in a slew of companies in the practice management space, such as rolling up dental or optometric businesses. The purchase prices were partially based on growth targets. The flaw in this model is that doctors may be good at treating patients, but they’re not as effective as growing the volume of patients.

Meanwhile, tariff policies have created volatility in supply chain costs which is impacting dealmaking in the logistics sector.

Continuation funds continue to be an option for PE firms, but they’re usually only viable for the most attractive companies in the portfolio rather than the ones offering lower growth.

Despite these challenges, optimism among dealmakers persists about a better exit environment for aging portfolio companies.

Justin King, partner at King & Spalding, said the middle market may be ripe for the “Great Trade Up,” referring to the idea that these PE shops may get to a point of actively looking to dump these assets to bigger PE firms or strategic buyers and move on.

“I’ve seen more and more sponsors in the middle market who are willing to part with these companies as they grow older – you rationalize doing it – you want to refresh the portfolio, you want to raise a new fund,” he said.

There are alternatives to unlock value, King said, such as the SPAC market for example.

What’s Next?

Brad Haller, senior partner at West Monroe, said private equity firms will curate a “renewed focus” on operational fitness, cost optimization and overall value creation at their older portfolio companies.

Dealmakers are also keeping an eye out for any changes in interest rate policy under the incoming Fed chairman. This could affect PE’s cost of capital and spark more interest in these older assets.

Overall, credit remains plentiful for deals, but interest rates are still not expected to drop to near zero, which is where they were prior to 2022.

For sure there are sectors that continue to perform well for PE-backed exits. Cybersecurity services and software businesses continue to draw strong interest from buyers in the middle market, including white collar services such as accounting and insurance, as well as residential and commercial services such as equipment maintenance and repairs.

“The commonality here is that there’s humans involved – someone who does your audit or someone replacing your furnace – there’s a human element involved here,” said Haller. “Those companies are drawing buyer interest.”