Few segments of the economy are as hot as data centers. Fast-spreading use of AI, on top of deepening digitization of business and daily life, means eye-watering demand for data processing. Growth is attracting huge volumes of capital, and M&A is flourishing as tech firms, real estate interests and utility providers jockey for advantage.

AI is one of the key trends that Frost & Sullivan has identified in the sector, says Nishchal Khorana, vice president. “AI is not just accelerating demand for new data centers, it is changing the nature of capabilities. We are seeing a significant shift in rack design for AI-ready data centers, from 6-8 kw racks to 50-100 kw racks.”

The emerging differentiation of AI-ready data centers is an important driver of M&A on several levels. For assets, some operators are focusing on AI-ready facilities and trying to divest their older operations. That opens the door for aggregators. In terms of geography, rural sites can be acquired and developed at lower costs than those in or near big cities where ultra-low latency is at a premium.

Blackstone (NYSE: BX) views AI and the digitization of the economy as a mega-trend that will drive demand for data centers. “Beyond investing in the construction and operation of actual data centers,” a firm spokesperson tells Mergers & Acquisitions, “we are active investors in utilities, renewable energy developers, battery storage technologies and other sectors and asset classes tangentially related to the growing demand for data centers.”

Blackstone cites a 2021 take-private deal in data center company QTS Realty Trust which it says has grown its lease capacity by 7x since the deal.

Balancing Real Estate and Connectivity

There are growing pains here, explains Kristina Metzger, vice chair of CBRE Data Center Capital Markets. Most markets are constrained by power transmission, not generation, for example.

“That can mean about four years for connection in Northern Virginia to more than 10 years in California,” she says. “Developers and operators can’t wait that long.”

Other pain points include water replacing air as the primary coolant system, which brings environmental concerns. Rezoning can also be contentious in developed areas. In Prince William County, Va., a Digital Gateway project advanced by QTS and Compass Datacenters has been met with a lawsuit filed by supporters of the Manassas National Battlefield Park, which runs adjacent to the project’s 2,000-acre development.

These issues are pushing development to secondary and tertiary markets. “We are seeing data centers coming to rural areas,” she says. “Access and time to power is the driver for remote locations.”

Industrial areas can be attractive because they already have substantial infrastructure. “Proximity to power plants could be a great advantage,” she says.

Theoretically, data centers could be anywhere, says Danny Freeman, senior partner in energy and utilities for West Monroe. “We are seeing them in more remote areas, but there are advantages to be near civilization.

“There are also opportunities in the utility supply chain,” says Freeman. “There is a huge backlog in transformers and heavy equipment, and there is a need for consolidation in both manufacturing and logistics. Private equity investors in particular are good at finding where industries are inefficient, and the utility supply chain is most inefficient.”

Among data centers themselves there has been some consolidation from within, with quite a bit public-to-private deals. Given how large some of the private ownership has gotten, Metzger reckons that there would likely have to be a public exit.

“We continue to see institutionalization,” she says, “including partial-interest ventures and recapitalization. There is so much diverse capital that there are lots of opportunities for investors to stay in the deal.”

The Next Consolidation Wave

Metzger stresses that data centers are unlike other asset types because they benefit from a diversity of capital. “We see infrastructure funds, real estate, project financing, as well as technology, media, telecommunications. It’s really across the spectrum, in contrast to other asset classes.”

Still, valuations have not gotten frothy. “These are long-term leases with fixed terms,” Metzger notes. “There is no direct mark-to-market, but bid-ask spreads have narrowed recently.”

Dealmaking in data centers is moving into its third phase, explains Khorana. “The telcos were the initial developers, because they had the fiber and the connectivity. The first phase of transactions saw a shift to carrier-neutral developers and operators. That led to a lot of M&A as facilities were acquired. Phase two was real estate interests. In phase three, investors of all kinds are infusing capital as the ecosystem comes together. There will be more M&A to accelerate time to market. Some operators may want to shed existing assets.”

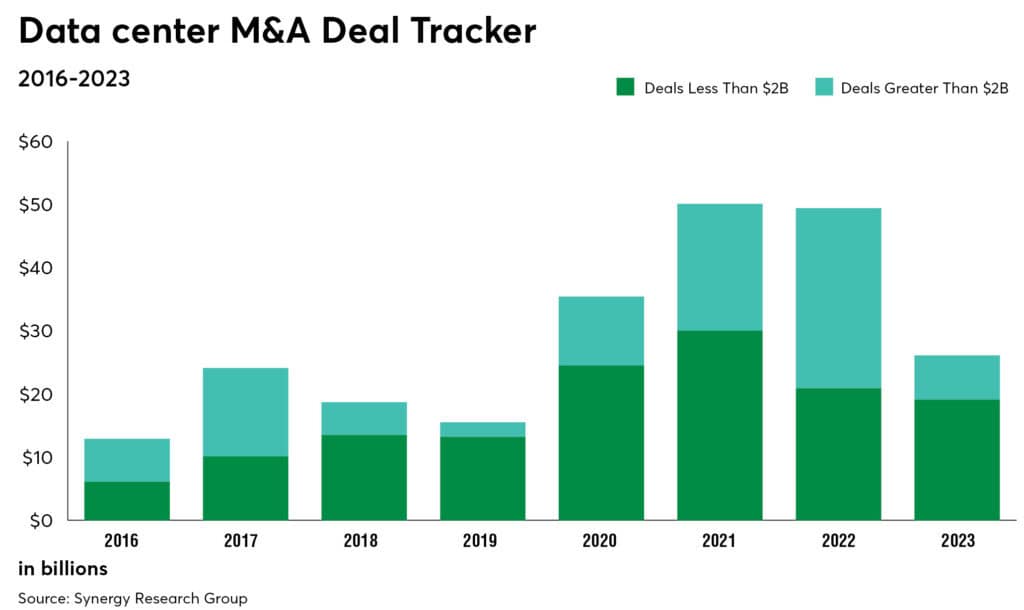

Total deals closed through August stood at $36.7 billion according to Synergy Research Group, with another $7.1 billion agreed but not yet closed. “We are aware of a pipeline of well over $20 billion in possible deals,” according to Synergy. “When some or all of those close – and taking into account the flow of deals which happen without prior notice — the final 2024 M&A figure could well match the high seen in 2021.” (See chart)

“There is definitely a consolidation play, especially in the middle market,” says Gabe Silva, a partner in the energy and infrastructure practice at Simpson Thacher & Bartlett. “We’ve done 40 to 50 deals of all sizes in the past few years. Many of the mid-sized operators are raising capital for organic growth as well as for acquisitions.”

Investors have capital to deploy and it is fueling activity across related sectors, adds Eli Hunt, Silva’s colleague and co-head of the group. “There is strong demand from data centers for services from other industries, including power and transmission, construction, equipment and especially for connectivity. That circles back to transmission and infrastructure.”

Silva notes that “some sponsors invest directly in data centers, while others are exploring how they can invest in ancillary businesses. Some data center operators are getting into self-generation, not only in the U.S. but also abroad.”

In all segments Silva says recent deals show the eagerness of private equity and infrastructure sponsors. “This sector is where value is being created across the board. We are seeing a lot of asset-backed financing as well as consortia of investors. GPs are now collaborating in some cases because of the growth and size of some of these platforms.”

Hunt adds, “there is interest from both private equity and from strategic companies. Investment is coming from infrastructure funds and real estate funds. The activity is a positive sign that data centers are trading, and are expected to continue to trade, at good valuations.”